This serves as a recap for myself and is not to be viewed as any kind of trade suggestion. All views expressed are my own.

Over the past week, we got a few delayed economic data points.

First one was the Non-farm payroll numbers, which showed strong job growth in Jan 2026, almost doubling the expectation. While at the same time, BLS published downward revisions of previous months employment numbers, causing some confusion as to the actual status of the economy and also perhaps calling into question the data integrity.

Then on Friday, CPI was revealed to show it was slightly below expectations and the feared Jan effect of a stronger inflation didn’t actually happen.

Taken together, I don’t think this changes the economy backdrop in any meaningful way. One thing that was changed was the expected rate cut schedule, now seen more likely for rates to stay at the current level until July of this year, delaying from June. But it also broadly confirms the current state of the low-hire-low-fire economy and that disinflation is running its course still with much feared tariff inflation not yet at least in the data.

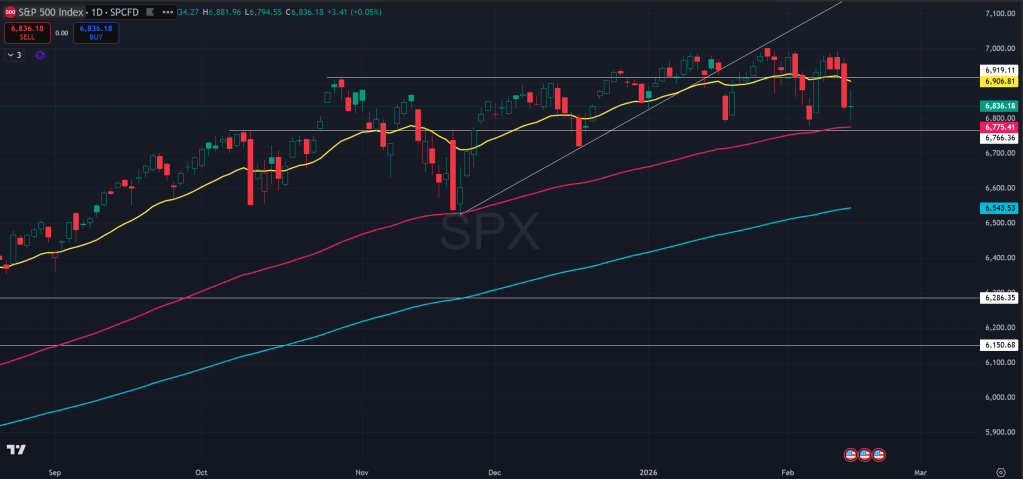

Price action wise for the SPX, it was very choppy last week. It is visible now that price has been stuck in an ever tightening range. On the daily level, price has been riding the 21EMA which at this point has started to turn lower, which does not bode well for the index.

We came close to hit the 100EMA on the daily which was hit last time late in 2025. SPX 7000 level has formed a very strong resistance level over the past few weeks and months.

Following the previous week’s turbulence and the rout in tech stocks, we saw some relief on Friday 2/6 but that relief did not translate to termination of the pullback and resumption of bull trend. Instead, price rejected the previous week high and made a lower high, which adds to reasoning for lower auction or at least continued chop.

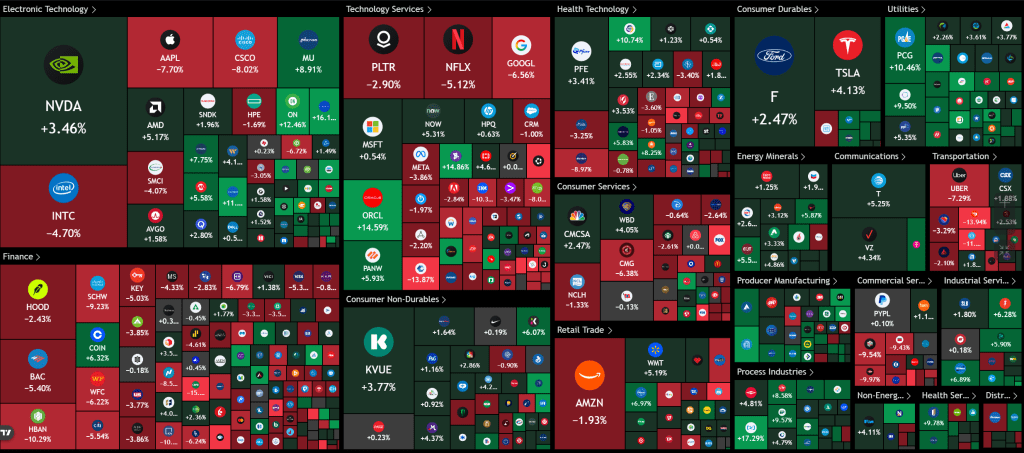

Under the hood, it is mostly a rotation out of the high flying stocks that gained so much in the past few years in the AI boom.

It’s interesting how narratives shifted. Before, it was AI going to benefit everything and everyone and be the next big thing that can boost productivity. Hyper-scalers and mega-caps were seen to stand to benefit the most from the AI boom.

Now, however, after seeing how much capital expenditure is needed to build out AI and the increasingly debt funded nature of said investments, people started to question if ever this AI arm’s race can sustain and bring the required return on such massive investments in reasonable time.

Another point of stress is in the concept of SaaS. It went from AI can help companies reduce operating costs and boost bottom line to AI might simply replace those software companies, rendering them obsolete and basically just grab their lunch.

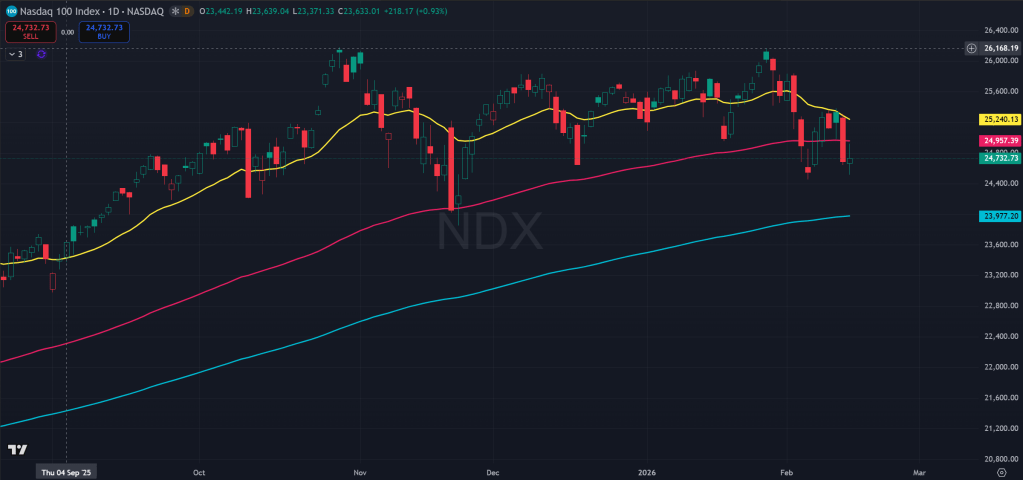

The result is a much weaker NDX relative to SPX and others. Within tech, hardware tech are still holding up relatively well, since the massive capex are still flowing for 2026 for memory chips and data center buildout.

But the benefits are mostly reaped elsewhere in other sectors like healthcare and industrials, where the AI can’t easily replace but can provide utility in increased productivity and boosting. Also these sectors are the ones that have lower multiples and hadn’t gotten as expensive as the tech sector.

To conclude, the economy is still holding pretty strongly with an almost goldilocks situation of still good labor market and disinflation running its course. There are concerns floating around with respect to AI expenditure and the debt and credit consequences as well as risks to the SaaS top and bottom line.

For the index, this likely means lower auction since it’s dominated by those big tech companies or at least extended chop while the rotation goes on underneath. This might continue on until we get more clarity into how those capex can turn into profits and who might ultimately emerge as the winner of the arm’s race.

The Ephemeral Tourist

February 16th. 2026 @ 2:46pm CST